Science-based expertise

One of the most important sustainability reporting developments in recent UK history has received official endorsement from the government. Following an initial show of support for the International Sustainability Standards Board (ISSB) framework , the Department for Business and Trade published the final UK Sustainability Reporting Standards on 25th February 2026. This UK sustainability reporting standards update marks a major step forward in the UK’s approach to sustainability reporting. This formal endorsement of the UK Sustainability Reporting Standards (UK SRS) aligns the UK with the ISSB and IFRS frameworks.

What the February 2026 Update Entails

At its core, the UK sustainability reporting standards update means the UK government has completed the endorsement process for the first two UK sustainability reporting standards.

- UK SRS S1 covers general requirements for disclosure of sustainability-related financial information

- UK SRS S2 focuses on climate-related disclosures.

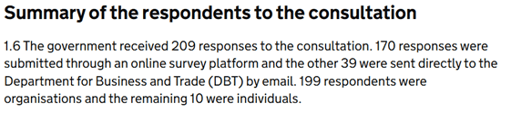

The standards were published on 25th February 2026 and are available for any entity to use voluntarily, either in full or in part. This matters because the UK did not simply announce broad support for international standards. It issued domestic versions of those standards, giving businesses a UK-branded reporting framework that is closely aligned with ISSB and the International Financial Reporting Standards (IFRS), but with targeted amendments aimed at the UK legal and regulatory context. That is the point at which high-level policy becomes something companies can actually benchmark against, plan for and implement. The government had earlier opened a consultation to fine-tune the final version of the guidance, this consultation drew 209 responses, 199 of them from organisations, and 88% of respondents who answered the key endorsement question supported endorsing UK SRS S1 and UK SRS S2.

Image credit: Gov.uk

How the UK SRS Fits into the Global Sustainability Reporting Landscape

Following COP 26 which took place in Glasgow, Scotland, the ISSB was created to serve as a global baseline for sustainability disclosures. The ISSB issued IFRS S1 and IFRS S2 on 26th June 2023.

- IFRS S1 sets general requirements for disclosing sustainability-related risks and opportunities

- IFRS S2 focuses specifically on climate-related disclosures

Both were designed to give investors decision-useful information and create greater consistency across capital markets. The UK’s approach has been to align with that global baseline rather than build a completely separate reporting system, with the government repeatedly describing the UK SRS as ‘being created by assessing and endorsing the global corporate reporting baseline of IFRS Sustainability Disclosure Standards’. In June 2025, the IFRS Foundation said that 36 jurisdictions had adopted, otherwise used, or were in the process of finalising steps towards introducing ISSB Standards into their regulatory frameworks. For internationally active UK groups, alignment with ISSB reduces the risk of having to build wholly separate sustainability reporting systems for different markets.

Key Differences: IFRS vs UK SRS

The government introduced targeted changes after considering consultation feedback, recommendations from the Technical Advisory Committee and Policy and Implementation Committee, and ISSB amendments published in December 2025. The most notable of these changes include the removal of specific time references for certain reliefs linked to non-climate reporting and Scope 3 emissions. In practical terms, voluntary adopters may use those reliefs indefinitely, while any future time limits for mandatory reporters would depend on later regulation or legislation.

Other key differences include:

| Area | IFRS Standards | UK SRS Adaptation |

| Effective date | Defined | Removed (set by regulators later) |

| Transition reliefs | Time-limited | Potentially ongoing for voluntary adopters |

| First-year reporting timeline | Flexibility allowed | Removed in UK version |

| Scope 3 emissions relief | Limited timeframe | No fixed end date |

| SASB Guidance | Mandatory tone | More flexible ('may' instead of 'shall') |

How Does this Impact Listed Companies

Listed issuers are most likely to feel the impact first. The Financial Conduct Authority (FCA) is already consulting on replacing its current TCFD-aligned listing rules with a framework that references UK SRS. The consultation closes on 20th March 2026, with the FCA aiming to publish a policy statement in autumn 2026 and bring rules into force from 1st January 2027. The FCA’s proposed model includes:

- Listed companies to report climate-related risks and opportunities in accordance with UK SRS S2, while using relevant provisions from UK SRS S1

- Scope 3 greenhouse gas emissions and wider sustainability-related risks and opportunities beyond climate would initially sit under a “comply or explain” approach

This gives boards and reporting teams a realistic preview of how mandatory UK SRS reporting may emerge: climate first, broader sustainability later, and with some proportionality in the earliest phases.

How Does this Impact Private Companies

The government has explicitly linked UK SRS to its Modernising Corporate Reporting programme, which will consider whether requirements should be introduced for private entities through the Companies Act. The government has also said it will consult later in 2026 on that wider programme. At this stage, reporting demand is likely to travel down the supply chain before formal legislation reaches every business directly. However, early preparation is key to ensure adherence to subsequent future legislations.

What’s the Difference Between the UK SRS and the EU CSRD?

The UK SRS and the EU’s Corporate Sustainability Reporting Directive (CSRD) are completely separate legislations. CSRD requires in-scope companies to report using European Sustainability Reporting Standards (ESRS), whereas UK SRS is the UK’s framework derived from ISSB standards.

Key differences

| Feature | UK SRS | EU CSRD |

| Region | UK | EU |

| Framework | ISSB/IFRS-based | ESRS |

| Status | Voluntary (for now) | Mandatory (phased) |

| Focus | Financial materiality | Double materiality |

This distinction matters because some UK-headquartered groups will face both UK and EU sustainability reporting pressures. In fact, the government’s consultation response itself noted that some respondents already had parent companies reporting under CSRD, and some asked for more guidance on interoperability between IFRS Sustainability Disclosure Standards and ESRS.

Learn More: CSRD Consulting

How Can Your Organisation Prepare for the UK SRS

The strongest response to this latest UK sustainability reporting standards update is to prepare in proportion to likely exposure.

Key priorities should include:

- Reviewing whether existing TCFD, SECR and broader sustainability reporting processes already provide a foundation for UK SRS readiness

- Conducting a gap assessment against UK SRS S2, especially on climate data, controls, governance and narrative reporting

- Assessing materiality processes, including how climate and broader sustainability-related risks and opportunities are identified and prioritised

- Deciding how scope 3 emissions data will be quantified, challenged and governed

- Establishing board-level and executive accountability for sustainability disclosures

- Monitoring the FCA consultation and the government’s later consultation on corporate reporting reform.

The Bottom Line

This UK sustainability reporting standards update move does not make reporting mandatory overnight, but it did settle the direction of travel: the UK now has a formal sustainability reporting baseline built on IFRS S1 and IFRS S2, and regulators are actively considering where and how it should be applied. Ensure your organisation is well prepared to meet any mandatory requirements from the UK SRS by booking a free consultation with one of our sustainability scientists to see how you may be affected.